What’s it all about?

A concept, typically used in factories, to ensure that when there is something limiting production that we prioritise the products that are going to make the greatest contribution. It has applications in all business situations though.

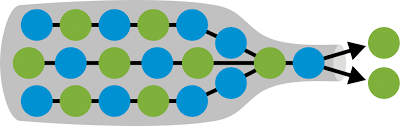

The idea would be to get all the production in your factory working in concert so that the product goes through all the stages at a constant speed. Much like all the soldiers arrive at the destination at the same time as they are in step.

The reality in a business process though is that not everything is in lockstep. It is more likely that there will be gaps forming because, even if everybody starts off at the same speed, individual variation, stride length, not stepping in exactly the same spot, carrying different weight etc. will mean that the line eventually strings out. I had plenty of experience trying to keep all my soldiers together when I was in the Army.

Photo Peter Shinn

If you think of each soldier as being a step in the manufacturing process, the process isn’t finished until the last soldier gets to the destination. The slowest soldier may not be the one at the back, he may be in the middle, but if no one can pass him, he is slowing down the whole process. Easy to keep everyone together in step on the parade ground, not so easy on rugged terrain.

That soldier is effectively a bottleneck (a constraint) under Throughput Accounting and the objective of this management accounting technique is to take action on the issues affecting ‘the slow soldier’ so that all get there at the same time.

Throughput Accounting is in essence this is ‘contribution per unit of limiting factor’ in another guise, applied to more complex situations than just a shortage of raw materials. Here it can be applied to circumstances where you can fix the shortage problem, because it is part of the process.

Most examples will be of Throughput Accounting (TA) applied to not having enough time on the machines in your factory to make everything (bottlenecks). This is because it is easier to understand and calculate in these scenarios, but it does apply in any situation where there is a process taking time, so it applies to services too.

It’s all about the bottlenecks.

If we don’t have enough time to make everything we want to make then we have a constraint, a limiting factor = the time available on the bottleneck.

The bottleneck in the process is the machine where there is not enough time to do all the work. If there is more than one bottleneck, then the one we are worried about is the biggest one. For the moment.

It is quite common to have one machine working on multiple products (at different times obviously). If that is a component for another product, then clearly you can’t complete the product without it. If you can’t complete it you can’t sell it. So, you can see it is critical that you get it made. We need to be making the critical components to finish production.

As the nursery rhyme says.

For Want of a Nail

For want of a nail the shoe was lost.

For want of a shoe the horse was lost.

For want of a horse the rider was lost.

For want of a rider the message was lost.

For want of a message the battle was lost.

For want of a battle the kingdom was lost.

And all for the want of a horseshoe nail.

The first mention of this rhyme around 1591,was apparently related to the death of King Richard III at Bosworth Field in 1485.

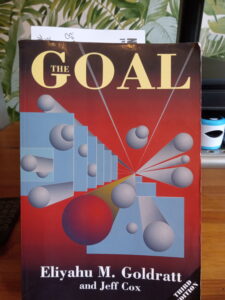

The concept of Throughput was introduced by Eli Goldratt in his novel The Goal.

An unusual way to teach Management Accounting, but in this instance an effective one. An entertaining read that covers all the principles.

The basic argument is that:

The objective of the business is to make money, to do that you have to sell product (send it to the customer), the capacity of the whole business is the capacity of the bottleneck, so everything has to be done at the speed of the bottleneck, there is no point making inventory as it is a liability not an asset, the only variable cost is Direct Material, everything else is Overhead.

Bottlenecks.

“A bottleneck,” Jonah continues, “is any resource whose capacity is equal to or less than the demand placed upon it. And a non-bottleneck is any resource whose capacity is greater than the demand placed on it. Got that?”

p 139. The Goal 3rd Edition

You may have designed your system at the optimal production rate, but it probably won’t happen in practice. A problem with a machine, an operative, poor training, downtime, difficulties with materials, all sorts of things can make a particular stage the bottleneck.

The fastest that can go, now determines the maximum rate that you can finish the product and the maximum you can earn.

“What you have learned is that the capacity of the plant is equal to the capacity of its bottlenecks,” says Jonah.”

p 158. The Goal 3rd Edition

This means that the entire cost of the factory (all the Overheads and Direct Labour) is covered by the work done on one machine (the bottleneck).

This is an unusual concept, but the one we use later when we prioritise production if the machine makes more than one product (as so often is the case in exam questions).

There is no point making more of the units before this stage (they’ll just pile up and they cost you money), and you won’t be able to make more after this stage than are made at the bottleneck.

What do we do about bottlenecks?

We don’t really want to live with them, after all it means we are not able to produce as much as we would like and that means we are not going to make as much money as we would like.

- Slow down.

There is no point having piles of partially finished work everywhere, so we will slow the whole process down. Not to the speed of the bottleneck machine, but a bit slower so that the backlog of partially completed work can be cleared. This may mean you have some people idle for a while, but that is better than making Work in Progress that you can’t finish.

- Fix the problem

Rarely is the bottleneck the fault of the person on that machine. it is much more likely to be a problem with the machine or the process. for machine, think of a photocopier that keeps jamming – it’s going to need repair or replacement. For process think about how you can make things run smoother by having a better designed process. is the person on the bottleneck slow because they have to do a task that could be done by someone else (e.g. do they have to open boxes? Could the components come to that machine unboxed. Anything that could save time? If it is the person, the most likely cause is inexperience or lack of training – train them!

- Speed up

Once you’ve solved the problem you can speed the whole process back up again until you have got to the maximum speed of that machine. It might still be the bottleneck in the process, but if not, you produce at the best speed – until there is a problem somewhere else!

If your bottleneck is still a bottleneck, then it is still restricting production and you have to plan your work to match this restriction.

Drum, Rope, Buffer.

This is one of Eli Goldratt’s concepts. It shows how you plan production to maximise the use of the bottleneck.

Loading...

Loading...

The Bottleneck is the machine that can do the least, machine D, which can only do 12 units per hour.

There is no point working faster than D as you will just build up work in progress in front of it (after A, B and C).

D is therefore the “drum”, its beat is the pace that the whole factory works at, 12 units per hour.

Machines E and F can’t work any faster than D as they are only getting 12 an hour, so they are slowed down too.

The amount of work at D determines how much should be released to A to work on. This is the rope. Stuff only goes into A at the pace that D is working. If D slowed down to 11 an hour, we would slow down the release of materials to A so that it also only did 11 an hour. If it sped up, then so would the feed to A.

If we slow A, B and C down to 12 an hour, there may be times when they produce fewer than 12.

So that D always has 12 to work on, we would have a buffer between C and D.

Some from C kept in here would allow D to continue working at 12 an hour if either A, B or C didn’t produce 12 an hour at some point for a short while.

We could also have a few kept in a buffer after F, before the product is sent to the customer, to make sure we can always supply 12 an hour.

That’s in case E or F fell below 12 an hour for some reason for a short period.

Seminar/Exam questions?

You might be asked about the principles, but I commonly see calculation questions based, not on the scenario described above, but on the situation where the bottleneck makes more than one product and they, therefore, need to be prioritised.

I’ll work through a question step by step to illustrate the calculations as we go along.

It is quite common to have a question with several machines requiring you to work out which is the bottleneck. Of course, the issue is the same if you already know which machine is your problem and you are prioritising the usage of that machine. You just don’t have to think about the other machines in your calculations.

Not just manufacturing.

Bottlenecks don’t just have to be points in a production process where stock levels are building up. In any business there might be a point where an individual or department is unable to deal with all the work coming their way. Work will be piling up, people beyond them in the process may not have enough to do and overall the business isn’t making as much as it should be.

Here too we go through the process of identifying the bottleneck, slowing down and prioritising what should be done while removing the constraint.

This vessel blocked the port at Littlehampton at the same time that the huge cargo ship blocked the Suez Canal.

The vessel that blocked the Suez Canal has even made it into painting. One I saw at a major exhibition of maritime art a year later.

Throughput accounting

This is the topic where we discus what you do when you have a bottleneck in the system. A stuck…

Posted by Management Accounting Info on Wednesday, 31 March 2021

“Stock is a symptom of inefficiency”.

There’s no point in making things you can’t sell and there is definitely no point in making things you can’t finish (Work in Progress). So we would scale back production to match the rate of the bottleneck machine. Remember, stock costs you money (the Direct Materials).

In calculation questions we try to use numbers that are easy to deal with. We don’t want to make our calculations unnecessarily complex. In reality, the the throughput through a production line is likely to be very high. Here 10,000 bottles of beer an hour.

Loading...

From Flavourly Magazine issue 45, Dec 2020.

Throughput accounting

This is the topic where we discus what you do when you have a bottleneck in the system. A stuck…

Posted by Management Accounting Info on Wednesday, 31 March 2021

I am not sure I agree…

Much of what I have read about Throughput Accounting, in other people’s interpretations, says that you don’t make a product if it’s TA Ratio is less than 1.0.

For example this comment from the ACCA:

“Where throughput accounting principles are applied, a product is worth producing and selling so long as its throughput return per bottleneck hour is greater than the production cost per throughput hour. This may be measured by the throughput accounting ratio. Where the ratio is less than 1·00, return exceeds cost and the focus should be on improving the size of the ratio.”

I just say, what happens if you stop making the product?

The only thing you save if you don’t make a product is the Direct Material costs of the product, and we’ve already taken those out of the equation as we are looking at Throughput (sales – direct materials). So, actually we don’t save anything. All the other costs are treated as Fixed. If you don’t make a product you are still going to spend the same amount of money on Labour and Overheads. Provided you’ve got a market you might as well carry on making things, at least you will get some income towards paying the Labour and Overheads.

Or am I missing something?

You can see a calculation that demonstrates this in my working demonstration above.

Reading

Curiously, this is a Management Accounting technique that was introduced to us in a novel.

Loading...

Information on Throughput Accounting from the ACCA.

Loading...

Loading...

Watch This.

Listen to these

Using the concept of Throughput Accounting in other situations is covered too in this series of podcasts. At least listen to the first so that you understand how a bottleneck can apply in any business, it’s not just about slow machines! Also a good summary explanation of bottlenecks at the end.

Podcast 1. Throughput. Steve Bragg from AccountingTools.com

The podcasts get more detailed as they go on, with good stuff in Part 5 for practical application in a factory (the controls and reports you need) to ensure you are maximising throughput. Beyond what you will probably need for your studies, but we are interested because we love management accounting!

Podcast 2. Throughput. Steve Bragg from AccountingTools.com

Podcast 3. Throughput. Steve Bragg from AccountingTools.com

Podcast 4. Throughput. Steve Bragg from AccountingTools.com

Podcast 5. Throughput. Steve Bragg from AccountingTools.com

Further Reading.

(Articles and news items related to this topic to put it in context for you). Remember, there may be some variation in terminology. Some use the term Return per Factory Hour (minute) rather than Throughput per Factory Hour (minute).

There are a range of things that can be restrictions/bottlenecks.

Here, this article talks about a number of issues that can be the restriction on work, not all of them due to physical issues that we can deal with through Throughput Accounting. they are real problems though and are solvable by taking the same approach as we have talked about for dealing with bottlenecks.

https://www.mmsonline.com/columns/where-is-your-herbie

March 2020. Chocolate Shortage! Oh no!

Elon Musk and Tesla.

Under pressure to produce the new Tesla on time the company has switched production from other lines and is working overtime. Not actually a bottleneck as we know it here as it isn’t one point of problem, but essentially the issues are the same.

The challenges faced by Tesla at the moment, trying to meet the level of demand give interesting examples of how it is possible to adjust production to meet targets. We’ve seen switching of resources (materials, money, labour) from other products, the expansion of facilities (working in additional temporary buildings) and overtime.

This is an example of reducing scope to simplify processes/save time.

Others

http://www.businessdictionary.com/definition/bottleneck.html

A bottleneck on the tube, the solution? Step 1. Slow the process down.

By only allowing standing passengers now arrive at the exit gate at the speed of the bottleneck (the exit gates). Step 2 is to solve the exit gate problem.

The consensus on this topic: https://en.wikipedia.org/wiki/Throughput_accounting

Here is a journal article that goes into developments in Throughput Accounting in some depth. Search on the title as there isn’t a pdf of the paper that I can share with you.

“Optimal product mix decisions based on the theory of constraints? exposing rarely emphasized premises of throughput accounting. emphasized premises of throughput accounting”

Rainer Souren * a, Heinz Ahnb & Christian Schmitzb. pages 361-374 International Journal of Production Research Volume 43, Issue 2, 2005

An example of how widespread the misunderstanding of the meaning of the TA Ratio is.

In case we haven’t covered it. A product with a TA Ratio of less than 1.0 is not losing money, it is still making a contribution. You will be worse off if you don’t make it.

Possible Written Questions.

(No indication of marks – the more marks a question gets, the more you are expected to write – detail that is, not just words!) If you can’t answer these, you need to do some more reading. I do ‘find’ questions elsewhere, so these aren’t all questions I have used myself.

What steps should a company take when they have identified a bottleneck in their processes?

Comment on the use of Throughput Accounting Ratios.

(Relating to calculations you will have just done in a Throughput Accounting question) – Explain how the method you have just used (TA) ensures that you make the most profitable product mix.

Explain whether you would cease production of any product that had a Throughput Accounting (TA) Ratio of less than 1.0.

Journal Article.

You may have to search your own library’s e-journal database to get access.

https://ideas.repec.org/a/ddj/fseeai/y2016i2p78-87.html