What’s it all about?

A technique for attempting to make sure that the costs of your product give you the profit you require at the price you intend to sell for.

When we look at Target Costing we are identifying the selling price and the profit margin that we require. This gives us a maximum cost that we can afford for production.

The ‘normal’ method is to work out your costs, then add a profit percentage so as to come up with the selling price. But what if nobody wants to buy at that price?

Target Costing works backwards from the selling price, determining how much you can spend to get your target.

If the actual cost will exceed this we then look at the various costs, the design/manufacture/overheads etc. to see what we can change to bring the cost down to the target.

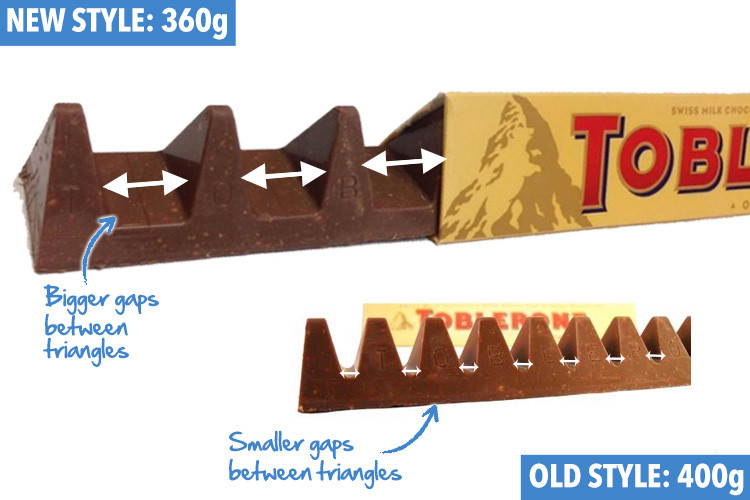

Look at how Toblerone maintained/improved their margins by changing the product.

Usually when a company reduces the quantity of product it sells for the same price it gets away with it. For Toblerone, the new design and reduction in chocolate was a bit too obvious.

Here they have reduced the chocolate content, by 10%, so their costs were reduced. Did the price come down 10% too? Thought not.

photo from The Sun newspaper

Coverage on the BBC with a video of customer responses:

http://www.bbc.co.uk/news/uk-37904703

And then it happened again in July 2020…

Pricing – Target Costing

Another example of ‘shrinkflation’ where companies maintain margins by reducing what they…

Posted by Management Accounting Info on Friday, 17 July 2020

Coverage of the changes to a number of chocolates in the last year. Interesting to see the companies’ responses to customer concerns. Some blame rising costs (essentially demonstrating Target Costing), others use marketing speak – one claims they did it to help combat obesity! If you don’t want me to be fat, stop making bloody chocolate then!

Target Costing summarised.

The Target Costing Process.

- Work out what the product will be, its precise specification and how many you think you will sell.

- Decide what you think you can sell it for successfully, that is, in enough quantity to be worthwhile. That’s your Target Selling Price.

- Work out how much money you want to make on every one you sell, that’s your Target Profit.

- Take the Target Profit from the Target Selling Price and this tells you what you can spend on making the product (providing the service). This is your Target Cost.

- Using your specification, work out what it will probably cost to make/provide. That’s your Estimated Production Cost.

- Take this estimated number from your Target Cost. You will almost certainly have a minus number, your Target Cost Gap. That’s how much more it is going to cost you now than you want it to.

- Do something to reduce the cost…..

Reducing Costs under Target Costing.

Clearly, if you are starting from scratch, there is more that you can do about reducing the cost of your product than if you have an established product. Change an established product and customers will notice – e.g. the derision over the re-costed Toblerone.

If you haven’t made it yet, you can change the specification and the customer won’t notice as they have never seen it before.

You do have to be careful that you don’t change the product so much that your Target Selling Price is no longer justified though.

You would normally have the Management Accountant working with marketing, production managers, quality control at least in making the decisions so as to ensure that you are not coming up with a cheap to make unsaleable product though.

It is about the design and manufacturing combining to reduce the cost without reducing the Use Value (how good it is at doing the important parts of its job), or the Esteem Value (what the customer is going to think of the product).

Design.

This is about changing the specification by making the product less complex with fewer components. It’s then cheaper to make because it has less ‘stuff’ to pay for and fewer steps to go through in the manufacturing process. Can a cheaper component be used instead? Can you use a standard item rather than a bespoke one for this product? Do we need that feature? If not, then perhaps we don’t need that component?

You can look at a product and think, what could I do without? If you can do without something, it will be cheaper to make. You may personally have products with lots of features you never use. Would you have still bought the product if it didn’t have that feature? Would you have even noticed?

Manufacturing

Better design reduces complexity and therefore the time taken to manufacture as well as the cost of materials. Can you use standard components that are widely used and therefore cheaper?

Can the product be machine assembled so reducing the cost of Labour? Can we train staff or redesign the Labour element to make them better at doing the assembly? (See The Learning Curve page for more on this aspect).

Can we reduce the cost of the materials by using cheaper without impacting on quality? Can we reduce the quantity of material used (the Toblerone approach)?

Watch This

Read This.

Target Costing

One of the ways that you can make sure that your product costs fall within your desired range so that…

Posted by Management Accounting Info on Tuesday, 5 January 2021

Possible Written Questions.

(No indication of marks – the more marks a question gets, the more you are expected to write – detail that is, not just words!) If you can’t answer these, you need to do some more reading. I do ‘find’ questions elsewhere, so these aren’t all questions I have used myself.

Explain the stages of the cost determination process in Target Costing.

How might a company reduce costs when the actual cost exceeds Target Cost?

What are the risks associated with reducing an actual cost to match Target Cost?

An example of a calculation question.

This is one a colleague used in the past. Note that the first part is a discussion around Target Costing. Once the calculations start, it is a straightforward Budgeting question (with a bit of loss in process/wastage thrown in).

I’ve given you this just so you can see how Target Costing questions, beyond discussion, are usually just standard Budgeting.

Loading...

Loading...